Insured Retirement Plans pair permanent life insurance with retirement planning to create tax-advantaged income. These plans grow through overfunded permanent life insurance policies like Whole Life and Universal Life options while maintaining death benefits. Corporations can establish similar arrangements through Corporate-Owned Life Insurance for executive benefits. The strategy offers tax-free wealth accumulation and policy loan access, though higher costs and potential surrender charges require consideration. Well-structured plans deliver tax-free retirement income and market volatility protection while managing risks of policy lapse or underperformance. Costs include mortality charges and administrative fees, offset by tax-deferred growth and tax-free distributions. Available in both the US and Canada (as Insurance Retirement Strategy), these plans provide pre-retirement liquidity and guaranteed income features that differ from RRSPs. With professional guidance and disciplined funding, Insured Retirement Plans share core concepts with Infinite Banking, both using life insurance for wealth building and financial control.

An insured retirement plan is a strategy that involves pairing a permanent life insurance policy with retirement planning to create tax-advantaged income. It is a strategy using a life insurance policy that includes a cash value component which, over time, grows on a tax-deferred basis. According to research from LIMRA, a leading research organization in the insurance industry, a properly structured insurance plan can be an effective tool for both protection and wealth accumulation when included as part of a comprehensive retirement strategy.

An insured retirement plan works by overfunding a permanent life insurance policy to maximize cash surrender value growth while maintaining the death benefit. The policyholder makes premium payments above the minimum required amount, with the excess directed to the policy’s cash value, which typically grows at 4-6% annually* depending on the policy type. According to research published in the Journal of Financial Planning, this strategy creates a financial vehicle that can later be accessed through policy loans or withdrawals without triggering taxable income, effectively creating tax-free income during retirement.

The types of insured retirement plans include various forms of Life Insurance such as Whole Life, Universal Life Insurance Policy, Indexed Universal Life, and Variable Universal Life policies. Whole Life offers guaranteed cash value growth rates averaging 1.5-3.5%* plus potential insurance dividend scales, while Universal Life provides market-linked returns typically capped between 9-13%* with downside protection.

Data from LIMRA’s Insurance Barometer Study shows that Universal Life Insurance has become increasingly popular for insurance retirement plans, with significant growth in this sector over the past decade.

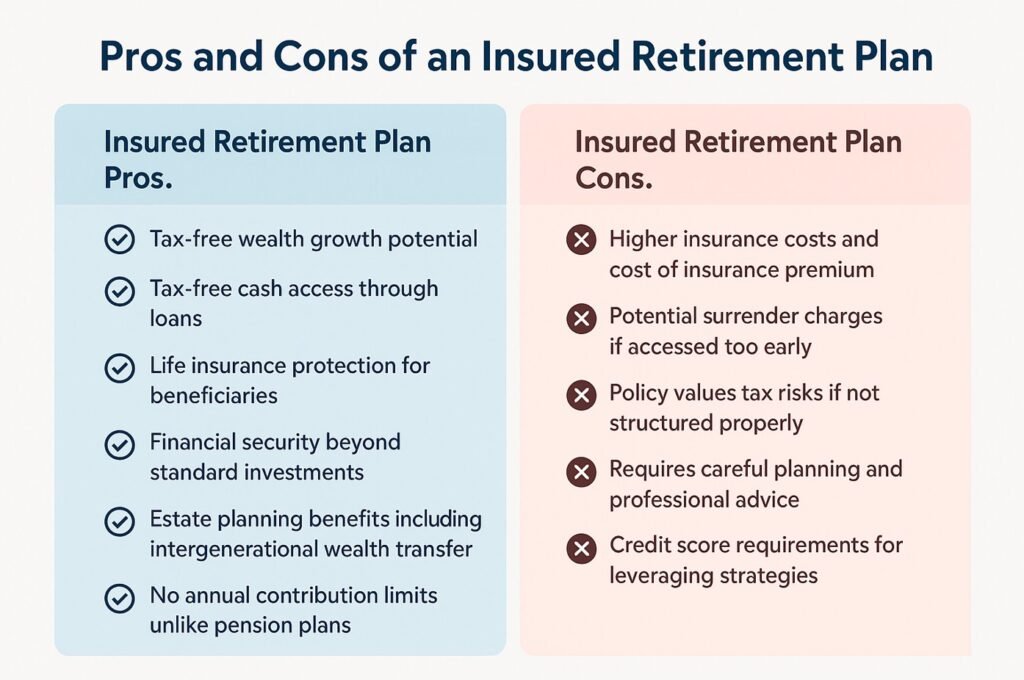

Tax-free wealth growth potential Tax-free cash access through loans Life insurance protection for beneficiaries Financial security beyond standard investments Estate planning benefits including intergenerational wealth transfer No annual contribution limits unlike pension plans Additional insurance protection through riders

Higher insurance costs and cost of insurance premium Potential surrender charges if accessed too early Policy values tax risks if not structured properly Requires careful planning and professional advice Credit score requirements for leveraging strategies According to Dr. Wade Pfau, Professor of Retirement Income at The American College of Financial Services and author of “Safety-First Retirement Planning,” retirement income strategies using insurance products can provide value for certain individuals, though the specific advantages depend on individual circumstances and proper implementation. Canadians should also be aware that improper structuring can jeopardize a policy’s exempt status under the Income Tax Act (Canada), resulting in unintended tax consequences as determined by the CRA.

Are There Corporate Insured Retirement Plans?

Corporate insured retirement plans do exist through arrangements like Corporate-Owned Life Insurance and Bank-Owned Life Insurance that provide tax benefits and supplemental executive benefits. According to research published by Deloitte, these plans represented over $142 billion in corporate surplus across Fortune 1000 companies in recent years, with a significant percentage of major corporations utilizing some form of corporate insured retirement plan program. These strategies remain effective tools for business owners seeking to fund non-qualified deferred compensation arrangements for key individuals in a dynamic business or family business.

The benefits of an insured retirement plan include tax-free income during retirement, protection from market downturns in your investment portfolio, financial legacy creation, and potential critical illness insurance benefits. Research from the Society of Actuaries indicates that properly structured plans can deliver significantly more disposable income compared to taxable investments due to tax advantages, with the added security of death benefits for economic security. These plans can provide protection against sequence-of-returns risk that traditional portfolios might not offer, helping maintain your desired standard of living and retirement lifestyle.

The risks of insured retirement plans include potential policy lapse, underperformance of investment component growth, high surrender charges, and insurance company insolvency. Data from the Canadian Life and Health Insurance Association (CLHIA) shows that a small but significant percentage of permanent life policies lapse within the first few years, with surrender charges often starting at 10-15%* and gradually decreasing over 10-15 years. The most significant risk is poor investment performance due to prolonged low interest rates, which has affected many policies issued in previous decades that failed to meet initial projections of investment growth.

Written by Jose Salloum, Financial Security Advisor, F.S.A., AIBP Authorized Infinite Banking Practitioner | IBC Financial — Canadian Wealth Creation Centre Last updated: April 2026

An insured retirement plan (IRP) is a Canadian financial strategy that pairs a permanent life insurance policy with retirement income planning to create tax-advantaged cash flow. In Canada, an IRP uses the tax-deferred growth provisions of the Income Tax Act (Canada), specifically Section 148 and the Exempt Test Policy rules under CRA Regulation 306, to accumulate cash value inside a life insurance policy that can later be accessed through policy loans without triggering immediate taxation. According to the Canadian Life and Health Insurance Association (CLHIA), permanent life insurance policies with cash value features remain one of the tools available to Canadians for supplemental retirement planning. IBC Financial, led by Jose Salloum, Authorized IBC Practitioner™, designs insured retirement strategies using participating whole life insurance for Canadian clients.

An insured retirement plan is a strategy that involves pairing a permanent life insurance policy with retirement planning to create tax-advantaged income in Canada. It uses a life insurance policy that includes a cash value component which, over time, grows on a tax-deferred basis under the Income Tax Act (Canada). According to research from LIMRA, a leading research organization in the insurance industry, a properly structured insurance plan can be an effective tool for both protection and wealth accumulation when included as part of a comprehensive retirement strategy.

An insured retirement plan works by overfunding a permanent life insurance policy to maximize cash surrender value growth while maintaining the death benefit. The policyholder makes premium payments above the minimum required amount, with the excess directed to the policy’s cash value, which typically grows at 4–6%\* annually depending on the policy type and dividend scale. This strategy creates a financial protection vehicle with cash value features that can later be accessed through policy loans without triggering taxable income under the Income Tax Act (Canada), provided the policy remains in force and maintains its exempt status under CRA Regulation 306.

The types of insured retirement plans available in Canada include strategies built on participating whole life insurance and universal life insurance policies. Participating whole life offers guaranteed cash value growth rates plus potential dividend participation from the insurance carrier’s participating fund. Universal life provides interest-crediting options that may include fixed-rate or index-linked returns, depending on the carrier and product design.

Data from LIMRA’s Insurance Barometer Study shows that permanent life insurance products with cash value features have maintained steady demand among Canadians seeking supplemental retirement income strategies. IBC Financial recommends participating whole life insurance from Canadian mutual insurance companies as the foundation for insured retirement planning, consistent with the Infinite Banking Concept.

Canadians should be aware that improper structuring can jeopardize a policy’s exempt status under the Income Tax Act (Canada), resulting in unintended tax consequences as determined by the CRA. Working with a licensed Financial Security Advisor experienced in insured retirement strategies is essential.

The benefits of an insured retirement plan include tax-free income during retirement through policy loans, protection from market downturns, financial legacy creation through the death benefit, and potential critical illness insurance benefits through optional riders. According to the CLHIA, properly structured plans can provide supplemental retirement income alongside registered accounts (RRSPs, TFSAs), with the added security of death benefits for beneficiaries. These plans can provide protection against sequence-of-returns risk that traditional market-based portfolios may not offer, helping maintain your desired standard of living and retirement lifestyle.

The risks of insured retirement plans include potential policy lapse if premium payments are not maintained, underperformance of cash value growth relative to projections, high surrender charges in the early policy years, and the rare but possible risk of insurance company insolvency. In Canada, Assuris — the industry-funded compensation corporation — protects policyholders up to specified limits if a member life insurance company fails. Surrender charges often start at 10–15% and gradually decrease over 10–15 years. These front-loaded expenses require a long-term commitment to overcome the initial cost basis and realize competitive returns.

Note: Dividend rates are not guaranteed. Past dividend declarations are not guarantees of future dividends. Cash value growth projections in any policy illustration are not guarantees of future performance.

The costs associated with insured retirement plans include mortality charges, administrative fees, premium loads, and surrender charges, collectively reducing returns by approximately 1.5–3.8% annually in the early years. These costs decrease as a percentage of total policy value as the cash value accumulates over time. IBC Financial provides detailed policy illustrations that show the year-by-year breakdown of all costs, guaranteed values, and projected values based on current dividend scales.

The tax advantages of insured retirement plans in Canada include tax-deferred cash value growth inside an exempt policy under the Income Tax Act (Canada), tax-free access to capital through policy loans when the policy remains in force, and income-tax-free death benefit payable to named beneficiaries. According to data published by the Canadian Life and Health Insurance Association (CLHIA), policyholders accessing income during retirement through policy loans can realize significant tax savings compared to fully taxable withdrawals from registered accounts. The tax treatment is governed by Section 148 of the Income Tax Act and the Exempt Test Policy rules under CRA Regulation 306.

Yes, insured retirement plans are available in Canada and are commonly referred to as insured retirement strategies or insurance retirement programs. In Canada, the strategy uses participating whole life insurance policies from federally regulated insurance carriers supervised by the Office of the Superintendent of Financial Institutions (OSFI). The tax framework that makes insured retirement plans effective is built into the Income Tax Act (Canada), specifically the provisions governing exempt life insurance policies and the tax treatment of policy loans. IBC Financial implements insured retirement strategies for Canadian clients using the Infinite Banking Concept framework.

Yes, you can use life insurance for retirement income in Canada through a properly structured insured retirement plan. The strategy involves accumulating cash value inside a participating whole life policy during your working years, then accessing that cash value through policy loans during retirement. Under the Income Tax Act (Canada), policy loans are not considered taxable income as long as the policy remains in force, making this an effective strategy for supplemental tax-free retirement cash flow.

Insured retirement cash flow is the systematic access of funds from a life insurance policy’s cash value through loans, partial surrenders, or dividends to create income during retirement years. The most tax-efficient approach in Canada uses policy loans rather than surrenders, because loans do not trigger a disposition under Section 148 of the Income Tax Act as long as the policy remains in force. IBC Financial designs insured retirement cash flow strategies that balance loan amounts against policy performance to ensure the policy remains sustainable throughout retirement.

You can access your funds before retirement in an insured retirement plan through policy loans, partial surrenders, or direct withdrawals at any age without age-based penalties. Unlike RRSPs, which trigger withholding tax upon early withdrawal and are fully taxable as income, life insurance policy loans in Canada can be accessed at any age without triggering immediate taxation, provided the policy remains in force and meets the CRA’s Exempt Test Policy requirements. This liquidity advantage of insured retirement plans provides penalty-free access to capital during working years for emergencies, opportunities, or major purchases that registered retirement accounts may not offer without tax consequences.

The guaranteed income options in insured retirement plans include the guaranteed cash surrender values contractually defined in the policy, which provide a floor below which your cash value cannot fall regardless of economic conditions. Additional income can come from non-guaranteed dividend participation and from policy loan strategies structured to provide systematic cash flow. IBC Financial designs guaranteed income components using the contractual guarantees within participating whole life policies issued by Canadian mutual insurance companies.

An insured retirement plan and an RRSP are fundamentally different financial vehicles. An RRSP provides an immediate tax deduction on contributions but all withdrawals are fully taxable as income. An insured retirement plan uses after-tax dollars to fund a life insurance policy whose cash value grows tax-deferred, and policy loans provide tax-free access to that cash value. RRSPs have annual contribution limits set by the CRA, while insured retirement plans have no government-imposed contribution limits beyond the Exempt Test Policy maximum. RRSPs must be converted to a RRIF by age 71 with mandatory minimum withdrawals, while insured retirement plans have no mandatory withdrawal requirements. Both strategies can work together — IBC Financial often recommends using RRSPs for their immediate tax deductions alongside an insured retirement plan for tax-free supplemental retirement income.

Building wealth with an insured retirement plan requires consistent premium payments over a long time horizon, ideally 15–20+ years before retirement. The strategy works by maximizing the Paid-Up Additions (PUA) rider to accelerate cash value growth while staying within CRA Exempt Test Policy limits. IBC Financial recommends starting as early as possible to take advantage of lower mortality charges and longer compounding periods. The wealth-building phase requires discipline — cash value accumulation is slower in the early years but accelerates significantly after year 8–10 as compound growth takes effect.

Insured retirement plans and the Infinite Banking Concept share core principles: both use participating whole life insurance policies as their foundation, both leverage the tax-deferred growth provisions of the Income Tax Act (Canada), and both provide access to capital through policy loans. Both offer a financial protection strategy with cash value features that serves as a complement to traditional registered accounts. In most Canadian provinces, both approaches can benefit from creditor protection for the cash value and death benefit when a preferred beneficiary — spouse, child, parent, or grandchild — is designated, as governed by provincial insurance legislation. Both espouse a disciplined philosophy centred on long-term planning and financial control.

The largest philosophical difference is that Infinite Banking is about being your own banker across your entire financial life, while insured retirement plans are more narrowly focused on retirement income planning. IBC Financial, led by Jose Salloum, Authorized IBC Practitioner™, implements both strategies for Canadian clients using participating whole life insurance from Canadian mutual insurance companies.

How much money do I need to start an insured retirement plan in Canada? Minimum effective premiums for an insured retirement plan typically start at $300–$500 per month, though the optimal amount depends on your age, health, income, and retirement goals. IBC Financial provides personalized policy illustrations that show projected cash value growth and retirement income based on your specific premium commitment.

Is an insured retirement plan better than an RRSP? An insured retirement plan and an RRSP serve different purposes and work best when used together. RRSPs provide immediate tax deductions, while insured retirement plans provide tax-free retirement income through policy loans. The best strategy depends on your marginal tax rate, retirement timeline, and overall financial plan. A licensed Financial Security Advisor can help you determine the right balance.

How long does it take for an insured retirement plan to build significant cash value? Most insured retirement plans require 7–10 years of consistent premium payments before cash value exceeds total premiums paid. The compounding phase begins after year 8–10, and the strategy works best with a 15–20+ year time horizon before retirement income is needed.

Are insured retirement plan policy loans taxable in Canada? Policy loans from an exempt life insurance policy are generally not taxable in Canada as long as the policy remains in force and maintains its exempt status under the Income Tax Act (Canada). If the policy is surrendered or lapses with an outstanding loan, a taxable policy gain may result under Section 148 of the Income Tax Act.

What happens to my insured retirement plan if I die? If you die with an insured retirement plan in force, your named beneficiaries receive the death benefit income-tax-free. Any outstanding policy loans are deducted from the death benefit before payment. The death benefit passes outside of probate when a named beneficiary is designated, which can provide significant estate planning advantages.

Book a free 30-minute IBC Discovery Meeting with Jose Salloum, Financial Security Advisor, to receive a personalized insured retirement plan illustration and analysis.

Phone: 438-808-3314 Email: Info@ibcfinancial.com Book Online: Schedule Your Free Discovery Meeting

*Disclaimer: Life insurance is not an investment product. An insured retirement plan is a financial strategy using life insurance — it is not a registered retirement plan and is not regulated as a securities product. \Dividend rates on participating whole life insurance policies are declared annually by each insurance company based on the performance of the participating fund. Dividends are not guaranteed. Illustrated rates in any policy illustration are not guarantees of future performance. Past dividend declarations are not guarantees of future dividends. The guaranteed values within a participating whole life policy (guaranteed death benefit, guaranteed cash surrender value) are contractually defined. Results vary based on individual circumstances, policy design, and insurance carrier. A licensed Financial Security Advisor can provide you with a personalized policy illustration under your specific circumstances. Jose Salloum is a licensed Financial Security Advisor regulated by the Autorité des marchés financiers (AMF) in Quebec. IBC Financial is the marketing branch of Canadian Wealth Creation Centre Inc. (CWCC).

Take the First Step to Financial Freedom!

We use cookies for analytics & functionality. Manage preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and Privacy Policy.

BannerText_Seraphinite Accelerator

BannerText_Seraphinite Accelerator